By the Cemex Ventures Investment Team | July 2026

The construction technology (ConTech) investment landscape delivered a strong signal in the second quarter of 2026: capital is back in motion. After a cautious start to the year, Q2 2026 closed with $1.031 billion in disclosed investment volume across 84 transactions, a 30% increase in deployed capital compared to Q2 2025. This resurgence, concentrated in productivity-enhancing technologies and AI-native startups, reflects a market that is becoming more selective, more strategic, and increasingly convinced that artificial intelligence is not a trend but a foundational transformation for the built environment.

At Cemex Ventures, we track global ConTech investment flows every quarter to map where innovation capital is going, and what it tells us about the future of construction. This report covers Q2 2026 data and full H1 2026 context, surfacing the key themes, geographies, and deal dynamics shaping the industry right now.

The headline numbers from Q2 2026 tell an interesting story. Investment volume jumped 30% year-over-year to just over $1 billion, yet the number of transactions fell 8%, from 92 deals in Q2 2025 to 84 in Q2 2026. This divergence between capital deployed and deal count points to a broader industry dynamic: investors are concentrating more capital into fewer, more mature bets. Check sizes are growing, diligence bars are rising, and the speculative flurry of earlier years has given way to conviction-driven deployment.

This is not a sign of weakness. It is a sign of maturity.

” ConTech deal activity remains within historical parameters and should not be interpreted as a sign of weakness. While transaction volume has declined compared to last year, we do not observe any meaningful market contraction. Instead, this moderation may be an indication of a maturing ecosystem, where investors are becoming more selective and concentrating capital in higher-quality opportunities. Overall, current activity levels remain healthy and do not raise concerns about the underlying strength of the sector. “ — Miguel Carralón, Investments & Partnerships Manager, Cemex Ventures

The ConTech ecosystem is shedding the excess of the 2021–2022 boom cycle and rebuilding around companies that can demonstrate real revenue, measurable ROI, and genuine product-market fit. The investors still writing checks, and they are writing larger ones, believe in the long-term thesis: construction is one of the world’s largest and least digitized industries, and the window to back the companies that will transform it remains wide open.

Zooming out to the full first half of 2026, total disclosed investment volume reached $2.884 billion across 153 transactions. On the surface, this represents a 19% decline in invested capital and a 20% drop in deal count versus H1 2025. But surface-level numbers require context.

Critically, the $2.884B figure excludes at least three major undisclosed acquisitions completed during the first half of the year. Incorporating reasonable estimates for these transactions, total H1 2026 investment volume is likely closer to $4.5 billion. The reduction in deal activity is real, but 153 transactions across six monthsreflects a healthy, active market.

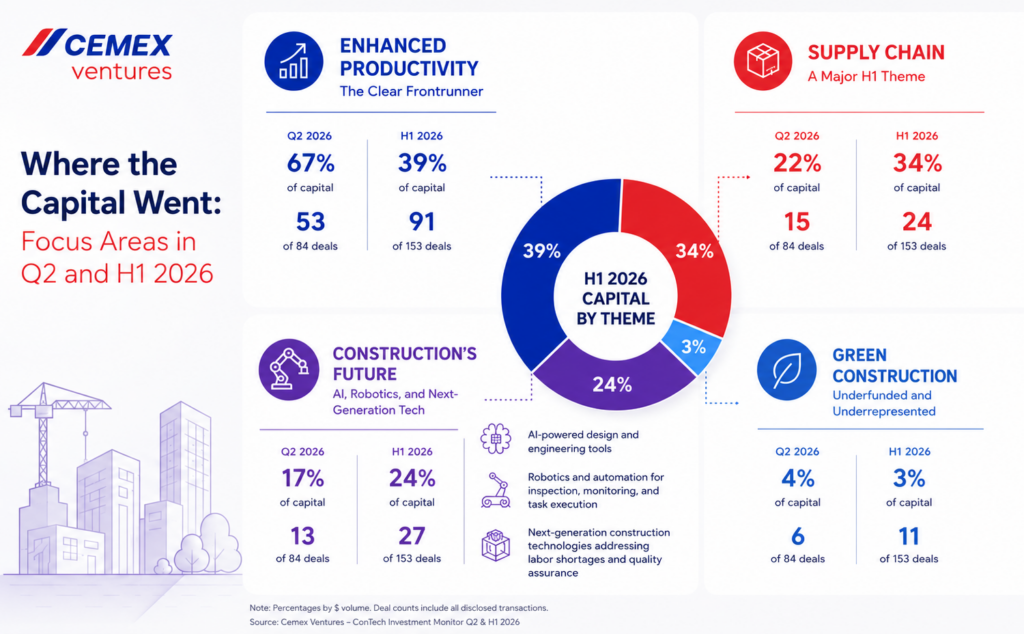

The dominant investment theme of Q2 2026, and the entire first half, was Enhanced Productivity. This category captured 67% of Q2 investment volume by dollar amount and 39% of H1 2026 capital. By deal count, Enhanced Productivity accounted for 53 of 84 transactions in Q2 and 91 of 153 in H1.

Investors are backing platforms that improve efficiency, automate repetitive workflows, digitize project execution, and reduce rework on construction sites. The appetite here is enormous, and it is easy to understand why: construction productivity has stagnated for decades relative to other industries. The companies solvingthis problem, whether through project management software, AI-powered scheduling, or digital twins, are addressing a genuine and urgent pain point for owners, contractors, and developers worldwide.

Supply Chain technologies emerged as the second-largest investment category in H1 2026, capturing 34% of invested capital and 24 transactions over the six month period. This reflects a sustained wave of investment in logistics optimization, procurement digitization, materials tracking, and supplier network management.

The construction supply chain remains one of the most fragmented and opaque in any major industry. Material delays, cost overruns, and lack of real-time visibility have long plagued projects at every scale. The startups attracting capital here are applying AI and data infrastructure to make the supply chain predictable, transparent, and responsive, capabilities the industry desperately needs.

“Supply chain is where projects are won or lost long before anyone sets foot on a jobsite. The surge of investment in this space reflects a growing understanding that digitizing procurement and logistics isn’t optional , it’s a competitive necessity for any serious contractor or developer.” — Jose Antonio Brunet, Principal, Cemex Ventures

The Construction’s Future category, encompassing AI-native design tools, robotics, autonomous systems, and advanced manufacturing, represented 17% of Q2 investment volume and 24% of H1 capital. With 13 deals in Q2 and 27 across H1, this category is punching above its weight in terms of strategic significance.

Three investment sub-themes stand out: AI-powered design and engineering tools that accelerate blueprint generation, optimize space utilization, and help ensure regulatory compliance; robotics and automation for inspection, monitoring, and task execution on jobsites; and next-generation construction technologiesaddressing labor shortages and quality assurance. These are the technologies that will define construction over the next decade.

Green Construction captured just 4% of Q2 investment volume (6 transactions) and 3% of H1 capital (11 deals). For an industry under significant pressure to decarbonize, and a regulatory environment in Europe and beyond that is tightening fast, this allocation remains strikingly low.

The opportunity is clear. The capital is not following it yet. This gap between sustainability imperative and investment reality is one of the defining tensions in ConTech right now, and one we expect to close as carbon reporting requirements, ESG mandates, and green procurement standards become unavoidable.

“Green Construction is still waiting for its inflection point. The regulatory pressure is mounting particularly in Europe; and the corporate sustainability commitments are real. The question is not whether capital will flow into this space, but when.” — Miguel Carralón, Investments & Partnerships Manager, Cemex Ventures

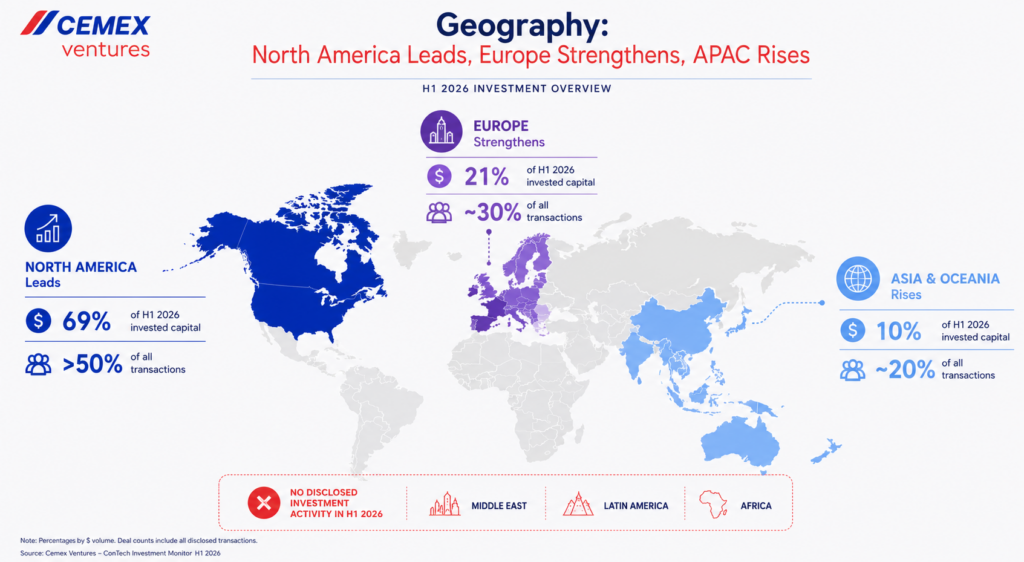

From a geographic perspective, the investment landscape remains heavily concentrated in three regions.

North America dominated H1 2026 with 69% of total invested capital and slightly more than half of all transactions. The U.S. market continues to lead in deal activity, check size, and the density of mature ConTech companies approaching growth and late-stage rounds. The concentration of strategic corporate investors and institutional venture capital in North America gives the ecosystem structural advantages that are difficult to replicate elsewhere in the short term.

Europe ranked second, attracting 21% of H1 invested capital and close to 30% of all deals. The gap between Europe’s share of capital (21%) and its share of deal count (approximately 30%) reflects smaller average deal sizes, but also a vibrant, diverse startup ecosystem spanning the UK, Germany, the Nordics, France, and the Iberian Peninsula. European ConTech continues to attract both local and cross-border investors, and the region’s strong regulatory push around sustainability and digitization is creating tailwinds for startups in green construction, compliance tech, and supply chain management.

Asia and Oceania accounted for 10% of H1 investment volume but nearly 20% of transactions, a pattern consistent with smaller deal sizes and a very active early-stage startup environment. Markets including Australia, Japan, Singapore, and India are generating significant entrepreneurial activity in construction digitization, and investor engagement in the region is deepening.

Notably, the Middle East, Latin America, and Africa recorded no disclosed investment activity in H1 2026. This does not necessarily mean deal activity is absent, it reflects limited public disclosure, but it does underscore the continued concentration of the tracked ConTech investment universe in three core geographies.

The breakdown of H1 2026 transactions by round type confirms that early-stage investing continues to dominate ConTech. Approximately 70% of all deals fell between Pre-Seed and Series A (108 transactions), while the remaining 30% corresponded to growth and later-stage rounds: 15 Series B, 2 Series C, 8 late-stagetransactions, 9 M&A deals, and 11 classified as other.

This distribution has two important implications. First, investors remain excited about the long-term opportunity in construction technology and are actively seeding the next generation of solutions, even as the overall funding environment has become more selective. Second, the pipeline of companies moving from early togrowth stage will determine whether H1 2026’s early-stage enthusiasm translates into a robust mid-stage ecosystem in 2027 and 2028.

The M&A activity is equally notable. Nine disclosed acquisitions in H1 2026 signal that the consolidation phase in ConTech is well underway, as larger platform players absorb specialized capabilities to strengthen their product suites.

Three strategic acquisitions during H1 2026 deserve particular attention because they reveal the strategic priorities of the industry’s largest platform providers.

Procore acquired DataGrid. Autodesk acquired Rhumbix. Trimble acquired Document Crunch. In all three cases, the acquirer targeted an AI-native company to strengthen a critical segment of its platform and embed artificial intelligence more deeply into construction workflows. These are not defensive acquisitions, they are offensive moves by companies that recognize AI integration as a competitive necessity.

And then there is the headline transaction of the period: Autodesk’s announced intention to acquire MaintainX for approximately $3.6 billion. This deal is a statement of strategic intent. Autodesk is no longer content to own design and preconstruction workflows; it wants to extend its platform into operations, facilitiesmanagement, asset lifecycle, and Industrial AI. For a company that has historically lived in the design phase, MaintainX gives Autodesk a credible foothold in the operational world that follows. If completed, this acquisition could fundamentally redefine Autodesk’s addressable market and intensify platform competitionacross the full construction lifecycle.

Perhaps the most striking data point from H1 2026 is this: approximately 70% of all ConTech transactions involved AI-enabled startups. This figure is not incidental, it is structural.

AI has stopped being a differentiator and started being a baseline expectation. Across Enhanced Productivity, Supply Chain, Construction’s Future, and even Green Construction, AI capabilities are being embedded into the core product architectures of the most fundable companies. Investors are no longer asking “does thisuse AI?” They are asking “how deeply is AI integrated, and how defensible is the resulting moat?”

Importantly, AI is not a separate vertical in ConTech, it is an enabling layer that cuts across every category. This distinction matters for how investors think about portfolio construction and how founders position their companies.

“We no longer evaluate startups by asking whether they use AI. We evaluate them by asking how central AI is to their defensibility. A company that has bolted on a chatbot is very different from one that has built its entire data and product architecture around AI capabilities from day one.” — Jose Antonio Brunet, Principal, Cemex Ventures

One of the most consequential trends in H1 2026 was the record level of participation from strategic corporate investors, who joined 37% of all transactions during the period. This is the highest level of corporate venture and strategic co-investment activity the ConTech market has seen.

Strategic investors, including construction companies, materials manufacturers, real estate developers, and engineering firms, bring more than capital to the table. They provide distribution, pilots, domain expertise, and market credibility that financial investors cannot replicate. Their growing presence signals that theconstruction industry itself is becoming a more active participant in shaping its own technological future, not merely a passive customer of innovation.

Where are strategics placing their bets?

The three investment themes gathering the interest from stratic investors are: project management and workflow optimization platforms that improve collaboration and data flow across the construction value chain; robotics and automation systems for inspection, monitoring, and task execution on active jobsites; and AI-powered design and engineering toolsthat accelerate blueprinting, support regulatory compliance, and optimize material consumption.

For startups, landing a strategic investor at an early stage has become a meaningful validation signal. For the ecosystem, it accelerates the path from pilot to deployment and helps close the gap between promising technology and real-world adoption.

Reading the Q2 and H1 2026 data together, several conclusions emerge:

The ConTech market is consolidating around quality. Fewer deals with larger check sizes reflect a flight to conviction. Companies that can demonstrate traction, unit economics, and scalability are attracting capital; those that cannot are finding the environment significantly harder.

AI is now the price of admission. Seventy percent AI penetration across transactions is not a coincidence. The companies raising capital are, in most cases, AI-native or AI-integrated by design. This will only accelerate.

Productivity, supply chain and new construction methods will remain the core investment thesis. Together, these categories accounted for amost all H1 capital. They address the industry’s most immediate and measurable pain points, and the total addressable market for both remains enormous.

Green Construction needs a catalyst. With 3% of H1 capital, sustainability-focused ConTech is significantly underfunded relative to the urgency of the decarbonization challenge. Regulatory pressure, net-zero commitments from major owners and developers, and maturing carbon accounting standards may provide thatcatalyst in H2 2026 and beyond.

The M&A wave is real and accelerating. The Autodesk-MaintainX deal alone represents a potential $3.6B transaction. Combined with the Procore, Trimble, and other strategic acquisitions, the platform consolidation narrative is becoming one of the defining stories in construction technology.

At Cemex Ventures, we remain committed to tracking, analyzing, and participating in the ConTech investment ecosystem. Q2 2026 confirmed what we have long believed: the construction industry is at an inflection point, and the companies building the technologies that will define its future are raising capital, findingcustomers, and scaling faster than ever.

The next wave of construction innovation is not coming. It is already here.

Construction Startup Competition has officially closed applications for its landmark 10th edition, reaching an unprecedented milestone with 798 startup applications from around the world, the highest number received since the competition was established in 2017. Compared to the previous edition, the competition achieved a 40.3% increase in applications, further strengthening its position as one of the world’s leading open innovation platforms dedicated to the construction industry.

The record-breaking edition reflects the accelerating pace of innovation across construction and sends a strong message to the market: the global ConTech and Cleantech ecosystem has never been more active. Increasing numbers of entrepreneurs are developing technologies that address the industry’s biggest challenges, while major corporations continue embracing open innovation as a strategic driver of transformation.

For the past decade, Construction Startup Competition has connected promising startups with leading construction companies, investors, and decision-makers worldwide. Beyond visibility, the initiative has become a launchpad for emerging companies looking to validate technologies, secure pilot opportunities, establish commercial partnerships, and scale internationally.

After a series of promotional events and a well-coordinated marketing and communications campaign, the Competition successfully attracted applications from 62 countries. A total of 64% of applicant startups are based in Europe and North America, while the remaining applications came from APAC (23%), Latin America (7%), the Middle East (5%), and Africa (1%).

“One of the most notable outcomes of this year’s edition was the 181% increase in applications from startups based in Asia and Oceania. This strong growth supports the Competition’s strategy of positioning itself as a gateway for APAC startups seeking to connect with leading global corporates, investors, and industry stakeholders, while expanding their reach into international markets,” said Miguel Carralón, Investment & Partnerships Manager.

This year’s edition focused on five new strategic innovation areas aligned with the priorities of the sponsoring partners, while also reflecting the challenges and opportunities that resonate most strongly with startups. Preconstruction Tech accounted for 21.7% of all applications, followed by Jobsite Productivity & Building Systems, which attracted 32.5% of submissions. ClimateTech for the Built World represented 22.8% of applications, while Smart Manufacturing & Logistics accounted for 9.9%. Finally, Smart Buildings & Infrastructure made up 13% of all applications received.

The distribution of applications across these focus areas highlights the growing industry demand for solutions that enhance productivity, accelerate digital transformation, improve sustainability, and drive greater efficiency throughout the built environment value chain.

Following the application phase, participating partners will now evaluate submissions before selecting the startups advancing to this year’s international Pitch Days in Singapore (IBEW), Las Vegas (Trimble Dimensions), and Helsinki (Recotech & Slush).

“Receiving 798 applications, and surpassing last year’s participation by more than 40%, is a remarkable achievement for the Construction Startup Competition and for the entire construction innovation ecosystem. Ten years ago, we launched this initiative with the ambition of connecting visionary entrepreneurs with the companies shaping the future of construction,” said Jesús Ortiz, Head of Cemex Ventures.

“Today, the record participation confirms that this vision is stronger than ever. It demonstrates not only the increasing relevance of the Competition, but also the growing maturity of the global ConTech ecosystem and the industry’s willingness to embrace innovation through collaboration. We are incredibly proud of what this platform has become over the past decade and excited to discover the technologies and founders that will define the next generation of construction.”

About Construction Startup Competition

Since its first edition in 2017, startups from more than 80 countries have participated in the biggest challenge aimed at startups in the construction industry, the Construction Startup Competition. Many startups have gone on to collaborate with the participating companies after applying to the Competition. Over ten editions, the initiative has established itself as one of the industry’s leading global open innovation platforms, connecting entrepreneurs with corporations, investors, and strategic partners to accelerate the adoption of breakthrough technologies across the built environment.

About Cemex Ventures

Launched in 2017, Cemex Ventures focuses on helping overcome the main challenges and capitalizing on the opportunity areas in the construction ecosystem through sustainable solutions. Cemex Ventures has developed an open collaborative platform to lead the revolution of the construction industry, engaging startups, entrepreneurs, universities, and other stakeholders to tackle the challenges in the construction environment and shape the industry’s future. For more information on Cemex Ventures, please visit: www.cemexventures.com.

About BCA

The Building and Construction Authority (BCA) champions a safe, sustainable, and liveable built environment for Singapore. As a leader in the sector, BCA is dedicated to driving industry transformation and setting rigorous standards in building safety, quality, and environmental sustainability. By advancing innovation, digitalisation, and the development of a skilled workforce, BCA fosters a dynamic industry that is ready to meet the evolving needs of the nation and build a resilient and progressive built environment for all. For more information, visit www.bca.gov.sg.

About Caterpillar Ventures

Caterpillar Ventures supports early-stage companies delivering innovative solutions in autonomy, robotics, energy transition, sustainability, and industrial technology. With the backing of Caterpillar Inc., we help founders turn breakthrough ideas into scalable impact across global industries. Visit caterpillar.com.

About Dysruptek

Formed in 2018, Dysruptek is the venture investment arm of The Haskell Company. Dysruptek seeks to invest in disruptive Architecture, Engineering and Construction technologies reshaping the built world. Invest. Invent. Innovate. For more information, please visit: www.dysruptek.com.

About Ferrovial

Ferrovial is one of the world’s leading infrastructure companies, operating in more than 15 countries with over 25,000 employees worldwide. For more information visit: www.ferrovial.com.

About Hilti Venture

Hilti Venture is the CVC arm of Hilti Group, investing globally in technologies transforming how the world is built, combining capital with strategic value and access to real-world jobsites. For more information visit: www.hilti.group.

About VINCI Group’s Leonard

Leonard is VINCI’s innovation and foresight platform, supporting startups and innovative projects in construction, mobility, energy and real estate. For more information visit: www.leonard.vinci.com.

About NOVA by Saint-Gobain

NOVA by Saint-Gobain is the venture capital arm of Saint-Gobain, supporting entrepreneurs advancing sustainability through strategic partnerships and investments. For more information visit: www.nova-saint-gobain.com.

About Trimble

Trimble is a global technology company connecting the physical and digital worlds to transform the way work gets done. For more information visit: www.trimble.com.

About Zacua Ventures

Zacua Ventures is an early-stage venture capital fund investing in Sustainability, Productivity and Urbanization across the built environment, supporting visionary entrepreneurs globally. For more information visit: www.zacuaventures.com.

For decades, construction has moved at the pace of its own certainties: blueprints, timelines, materials, and labor. That equation is changing now, and not as a passing trend. Technology is entering every phase of a project’s life cycle, from the first line drawn in design software to the sensor monitoring a bridge twenty years after it opens, and it’s redefining what it means to build well.

At Cemex Ventures, we’ve spent years watching this shift up close. Not as spectators, but as active investors in the startups driving it. This year, with the Construction Startup Competition 2026 (CSC26), we’ve defined five verticals that together map out the most complete picture yet of where this industry is headed: Preconstruction Tech, Jobsite Productivity & Building Systems, ClimaTech for the Built World, Smart Manufacturing & Logistics, and Smart Buildings & Infrastructure.

Let’s walk through each one. And at the end, we’ll tell you how your startup can be part of this conversation.

Every construction project is largely decided before construction even begins. The precision of a cost estimate, a risk assessment, or a permitting process determines whether a project turns a profit or becomes a financial sinkhole.

That’s why the first CSC26 vertical focuses on Preconstruction Tech: technologies that use data and analytics to improve decision-making before a project breaks ground. This covers BIM and digital twins, cost estimation and budgeting, document management, payment and finance, permitting and compliance, planning and scheduling, risk assessment and scenario planning, site analysis and feasibility, and tendering and bid management.

The shared goal across all of these solutions is clear: reduce uncertainty. The earlier a construction company can anticipate a cost overrun, a delay, or a regulatory risk, the more room it has to course-correct. The startups building in this space aren’t just digitizing old paper-based processes — they’re giving the industry something it never had at this scale: predictive visibility.

Once a project breaks ground, the challenge shifts entirely. It’s no longer about deciding — it’s about executing well, with the right resources, at the right time, without costly mistakes.

The second vertical, Jobsite Productivity & Building Systems, brings together everything that helps a jobsite function as a coordinated system: 3D printing, alternative construction systems, AR/VR for training, equipment tracking, field data capture and reporting, geotechnical analysis, industrialized and automated construction (offsite, modular, precast), jobsite robotics and automation, productivity analytics, progress tracking and site intelligence, project management, quality control and inspection, safety management, and workforce management.

What’s interesting about this vertical is that it tackles one of the industry’s most persistent problems: the productivity gap compared to other sectors. Construction has been slow to adopt automation and real-time data, but the startups competing here are proving that gap can close — one jobsite, one data point at a time.

The built environment is one of the planet’s largest consumers of resources and sources of emissions. But beyond the number you already know, what matters right now is what’s happening on the ground: tightening regulations, net-zero targets with real deadlines, and clients who no longer accept “that’s how it’s always been done” as an answer.

ClimaTech for the Built World brings together the technologies capable of meeting that pressure without sacrificing performance or cost: alternative fuels and new energy sources, carbon tools and calculators, carbon capture, utilization and storage (CCUS), circular construction and waste management, energy efficiency, environmental conservation and mitigation, machinery electrification, SCMs and material enhancers, sustainable materials, sustainable product libraries and life cycle assessment (LCA) tools, and water efficiency and management.

What sets the winning startups in this space apart is that they don’t pitch sustainability as an ethical add-on — they pitch it as a business lever: materials that cost less over time, processes that consume less energy, buildings that depreciate more slowly because they’re built to last and built to comply.

Construction no longer starts or ends at the jobsite. Increasingly, value is created in manufacturing plants, quarries, warehouses, and logistics routes that feed into projects.

That’s where the fourth vertical, Smart Manufacturing & Logistics, comes in: advanced materials, digital twins of industrial assets, energy optimization in industrial processes, fleet management for raw material extraction, industrial IoT, optimization of materials manufacturing (mixes, coatings, binders), optimized control systems, predictive maintenance for heavy equipment, process analytics and AI optimization, quality control and material consistency, quarry and mining operations management, delivery solutions, fleet management and logistics optimization, inventory management, marketplaces for equipment and materials, procurement and supplier management, and warehouse automation.

This vertical connects directly to something we’re already seeing across the Cemex Ventures ecosystem: the line between construction and heavy industry is blurring. Startups that understand both worlds — how things are manufactured and how things get built — hold a major competitive edge.

Finally, the fifth vertical looks beyond handover day. A building or a piece of infrastructure doesn’t end when it opens — it begins an operational life that can last decades, and that life can be optimized too.

Smart Buildings and Infrastructure brings together connected systems, sensors, and data that make it possible to operate and maintain assets more efficiently, safely, and intelligently: asset management, building management systems (BMS), digital twins in the operations phase, energy management systems, facility management platforms, infrastructure monitoring (bridges, roads), performance management, smart cities and connected infrastructure, and smart sensors and IoT integration.

Here, the challenge isn’t building better — it’s operating better what’s already built. And since most of the world’s buildings and infrastructure already exist, the market potential for these solutions is, quite simply, enormous.

If these five verticals prove anything together, it’s that the future of construction won’t be defined by a single disruptive technology, but by the sum of many innovations working across different phases of a project’s life cycle. From the decision to invest in a plot of land to the sensor that flags a crack in a bridge thirty years later, every phase has room to improve — and every improvement compounds with the rest.

That’s exactly the vision behind the Construction Startup Competition, the flagship program from Cemex Ventures and Zacua Ventures to identify, connect with, and invest in the startups building this new industry. Since its first edition, CSC has been a meeting point between founders with real solutions and the industry players — builders, manufacturers, operators, and investors — who need those solutions to stay competitive.

The CSC26 edition arrives with these five updated verticals precisely to reflect where innovation actually lives today: not in silos, but in an interconnected ecosystem where preconstruction, execution, sustainability, manufacturing, and operations all feed into one another.

For a growth-stage startup, joining CSC26 isn’t just a visibility opportunity. It’s direct access to:

It doesn’t matter whether your startup fits neatly into one vertical or crosses several of them, as the most interesting innovation often does. What matters is that you’re solving a real industry problem with technology that already works, or is close to working, at scale.

If your startup operates in any of these five verticals — Preconstruction Tech, Jobsite Productivity & Building Systems, ClimaTech for the Built World, Smart Manufacturing & Logistics, or Smart Buildings & Infrastructure — now is the time to take the step.

Applications for the Construction Startup Competition 2026 close on June 28th.

This deadline isn’t flexible. Selected startups will move directly into an evaluation process with the Cemex Ventures and Zacua Ventures team, and only those who apply on time will get that chance.

Cemex has been named a Global Innovator at the 6th Annual BuiltWorlds Global Innovators Awards. Explore the recognition, context, and Cemex Ventures’ track record of industry-leading innovation in construction technology.

Cemex has once again earned its place among the world’s most forward-thinking organizations in the built environment. At the 6th Annual BuiltWorlds Global Innovators Awards, Cemex was named one of the Global Innovators Top 50— a prestigious list that spotlights fifty companies from around the world driving the digital transformation of construction and infrastructure.

This recognition is more than a badge of honor. It is a reflection of a sustained, deliberate commitment to innovation that Cemex Ventures has been building since its founding in 2017.

BuiltWorlds is one of the leading research and events organizations in the Architecture, Engineering, and Construction (AEC) sector. Each year, it publishes the Global Innovators list to recognize organizations that are actively shaping the future of the built environment through technology adoption, investment, and digital transformation.

Now in its sixth edition, the award has evolved into one of the most respected benchmarks of innovation leadership in the global construction industry. This year’s honorees were selected based on their strategic moves in digitalization, sustainability, and technology deployment across the asset lifecycle, from design and procurement through construction, operations, and maintenance.

As Audrey Lynch, Director of Research at BuiltWorlds, noted about this year’s cohort: the recognized companies represent the very best of the industry’s efforts to improve how we build and operate structures and infrastructure.

Cemex Ventures was launched in 2017 as the open innovation and corporate venture capital (CVC) arm of Cemex. Since then, it has grown into one of the most active investors and innovation catalysts in the global construction technology ecosystem.

With investments in over 25 companies across the AEC space, Cemex Ventures has built a portfolio that directly supports Cemex’s broader “Future in Action” net-zero roadmap. The strategy is clear: back startups that can deliver measurable environmental and operational impact, and integrate those solutions across Cemex’s operations in the Americas and Europe.

The 2026 Global Innovators recognition is part of a growing pattern of external validation for Cemex’s innovation leadership. Here is a timeline of key accolades:

Cemex Ventures was featured in BuiltWorlds’ 5th Annual Global Innovators list, recognized as one of the most active investors and innovators in the built world, with particular mention of its Startup Competition and CVC activities in construction tech and industry 4.0.

Cemex was recognized among the Top 100 Corporate Startup Stars for two consecutive years — 2023 and 2024 — in the annual celebration of best global practices in open innovation, organized by the International Chamber of Commerce (ICC) and Mind the Bridge. In 2023, Cemex additionally received the Special Award: CVC to Deploy Sustainable Construction, acknowledging its outstanding role in fostering corporate-startup collaboration focused on sustainability.

In one of its most significant recognitions to date, Cemex Ventures was named Sustainability Investor of the Year at the BuiltWorlds 2025 Investor Awards. The award was presented to Jesús Ortiz, representing Cemex Ventures, during a ceremony that brought together global leaders in infrastructure and construction technology. The recognition specifically acknowledged the firm’s growing portfolio of startups focused on climate solutions, digitalization, and advanced construction technologies — including its strategic investment in Terra CO2, whose OPUS SCM product can reduce cement-related emissions by up to 70%.

The most recent recognition. Cemex has been named one of the 50 leading global organizations advancing the future of the built environment at the 6th Annual BuiltWorlds Global Innovators Awards.

The construction industry stands at an inflection point. Governments are ramping up investment in transport, energy, and urban infrastructure. At the same time, the sector faces mounting pressure to decarbonize, digitize, and improve productivity, challenges that cannot be solved with yesterday’s tools.

For Cemex Ventures, innovation is not a side initiative. As we firmly believe at Cemex Ventures: innovation is no longer optional for the industry , it is the operating layer behind productivity, sustainability, and scalability across the built world.

Companies that integrate technology effectively are increasingly setting the pace for the rest of the industry. Being recognized on the Global Innovators list is a signal that Cemex is not just adapting to the future of construction — it is helping to define it.

The conversation doesn’t stop here. Cemex will be represented at the upcoming #ParisGlobalSummit hosted by BuiltWorlds, where leaders from across the global construction ecosystem, startups, corporates, investors, and innovators, come together to accelerate the adoption of transformative technologies.

It’s a fitting stage for a company that has spent nearly a decade proving that construction can be smarter, cleaner, and more connected.

Construction Startup Competition 2026 is officially open, marking the 10th edition of one of the construction industry’s leading global platforms for startups advancing innovation across the built environment. This year, Cemex Ventures, Caterpillar, Dysruptek by Haskell, Hilti, Leonard by VINCI Group, NOVA by Saint-Gobain, BCA, Trimble, and Zacua Ventures once again join forces to identify and support the next wave of high-potential startups transforming the way the world builds.

Now in its landmark 10th edition, the Competition continues to connect emerging companies with leading organizations, investors, and industry decision-makers seeking scalable solutions to some of construction’s most pressing challenges. Startups selected for the program will gain access to strategic visibility, valuable industry connections, potential pilot opportunities, and exposure to capital partners across a global innovation ecosystem.

This year’s Construction Startup Competition 10th edition introduces five strategic focus areas aligned with the sector’s evolving priorities: Preconstruction Tech, Jobsite Productivity & Building Systems, ClimaTech for the Built World, Smart Manufacturing & Logistics, and Smart Buildings & Infrastructure. Through these categories, the Competition aims to spotlight the technologies driving greater efficiency, resilience, sustainability, and performance across the construction value chain.

To mark its 10th anniversary, Construction Startup Competition 2026 will conclude with three flagship Pitch Days designed to connect startups with regional innovation hubs and global industry leaders. Finalists will have the opportunity to present their solutions in Singapore, Helsinki, and Las Vegas.

Over the past decade, Construction Startup Competition has become a recognized launchpad for startups seeking to scale internationally, validate their technologies with leading industry players, and unlock new business opportunities. Its strong global network and track record of fostering collaboration between startups, investors, and corporates have positioned the Competition as a key platform for innovation in construction.

“The 10th edition of the Construction Startup Competition reflects both the scale of the opportunity ahead for construction innovation and our continued commitment to the talent shaping its future. For startups, this competition represents far more than visibility; it is a gateway to strategic industry exposure, meaningful connections, and tangible opportunities for growth. At Cemex Ventures, we believe the future of construction will be built by bold entrepreneurs, and this platform is one of the ways we help bring that future closer,” said Jesús Ortiz, Head of Cemex Ventures.

As the construction industry continues to evolve, a new generation of ConTech and Cleantech innovators is being called to redefine how the sector designs, builds, and operates. Startups from around the world are invited to apply and become part of a global platform built to accelerate the solutions shaping the future of construction.

Official Website: https://constructionstartupcompetition.tech/

The construction technology (ConTech) investment landscape entered 2026 with a mix of resilience and recalibration. In Q1 2026, a total of $1.85 billion was deployed across 68 transactions, broadly aligning with capital deployment levels observed overrecent quarters.

However, this apparent stability masks a deeper shift: investment activity declined 33% year-on-year, both in terms of capital invested and number of deals. This signals not a contraction of the market, but a continued normalization and increasedselectivity in capital allocation.

Q1 2026 stands as the weakest quarter since Q1 2024, reinforcing a broader trend already visible throughout 2025: investors are prioritizing quality over quantity.

This is consistent with wider venture capital dynamics. Across sectors, capital has become more disciplined following the post-2021 correction, with stronger emphasis on:

In construction specifically, this translates into a sharper focus on technologies that deliver measurable impact on cost, time, and productivity.

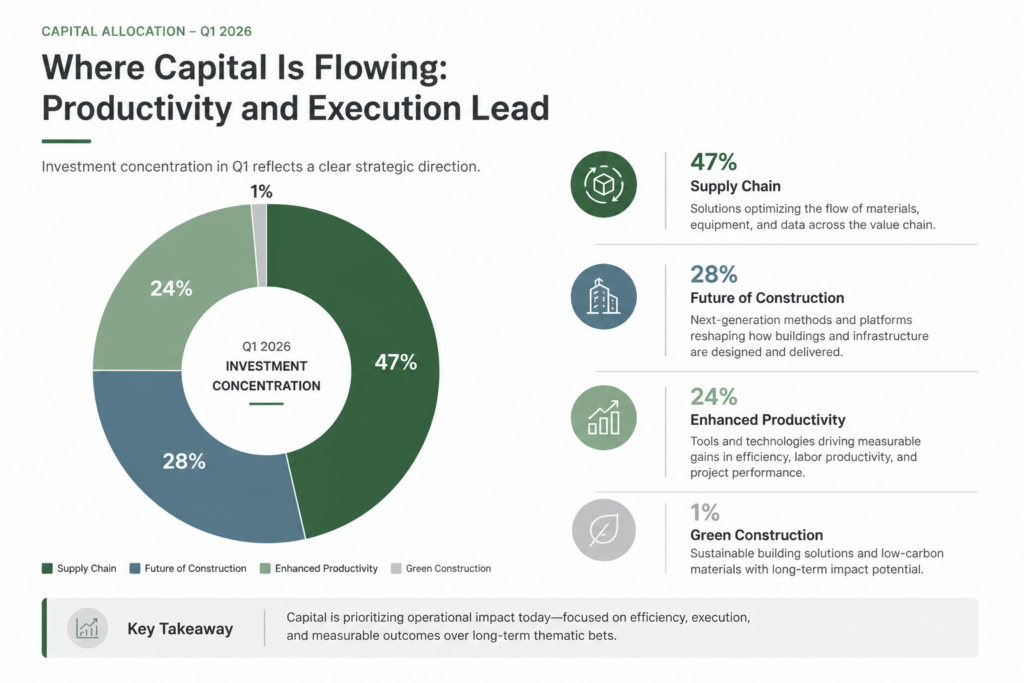

Investment concentration in Q1 reflects a clear strategic direction:

The dominance of supply chain and productivity-related solutions highlights a structural shift. Rather than focusing primarily onlong-term sustainability bets, investors are prioritizing immediate operational efficiency and resilience.

This does not imply reduced importance of decarbonization. Instead, it suggests that climate solutions are being evaluatedunder stricter commercial and industrial viability criteria.

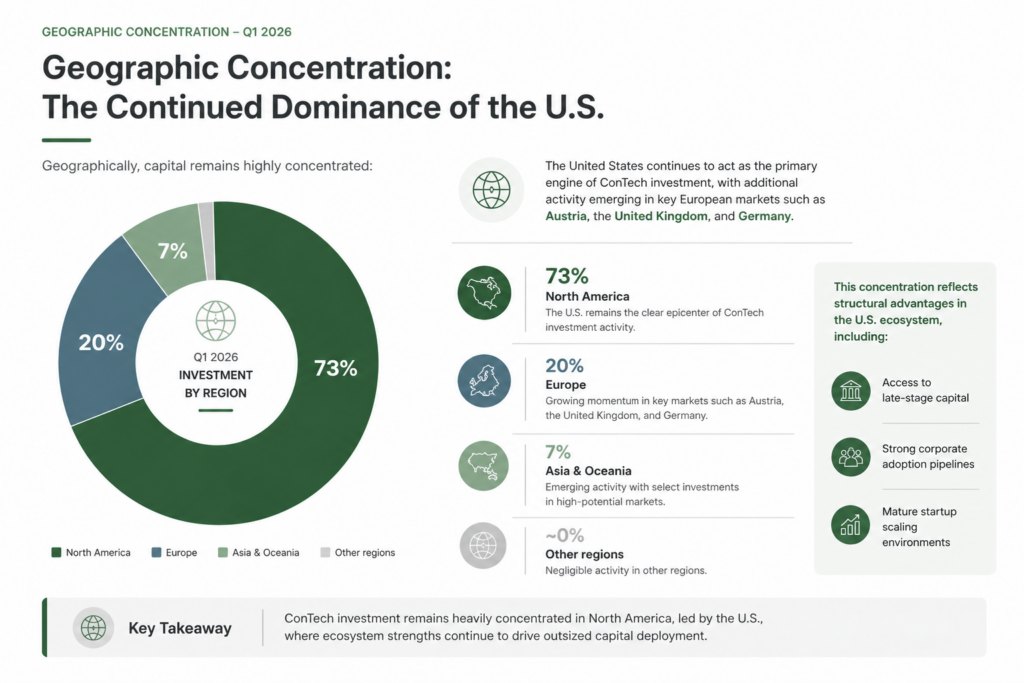

Geographically, capital remains highly concentrated:

The United States continues to act as the primary engine of ConTech investment, with additional activity emerging in keyEuropean markets such as Austria, the United Kingdom, and Germany.

This concentration reflects structural advantages in the U.S. ecosystem, including:

Despite the presence of large headline deals, 80% of transactions occurred between pre-seed and Series A.

This indicates that innovation pipelines remain active, with a continuous influx of new startups addressing persistent industrychallenges. At the same time, it reinforces the idea that capital is being deployed cautiously at later stages, favoring fewer butlarger, high-conviction bets.

Strategic investors participated in 35% of all transactions, underscoring the ongoing relevance of corporate venture capital in theecosystem.

A clear example is Cemex Ventures’ investment in WtEnergy Advanced Solutions, reflecting continued commitment totechnologies that can transform industrial processes and support decarbonization efforts.

The three major tech contech giants (Autodesk, Procore, and Trimble) were also active on the M&A front, acquiring Rhumbix, Datagrid, and DocumentCrunch respectively, further reinforcing their commitment to native AI‑driven solutions. * Although the DocumentCrunch acquisition was reported in April, we believe it is still worth highlighting.

This sustained engagement suggests that corporates are not retreating, but rather doubling down on targeted, high-impactinnovation.

One of the most defining trends of the quarter is the role of artificial intelligence:

AI is no longer perceived as a differentiator. Instead, it has become a foundational capability embedded across the entireConTech stack, from:

This evolution marks a critical shift: the competitive advantage is no longer in using AI, but in how effectively it is integrated intoworkflows and decision-making processes.

Several high-profile deals in Q1 illustrate where the market is heading:

These transactions reinforce three key patterns:

Despite macroeconomic uncertainty—driven by geopolitical tensions and persistent inflationary pressures—the outlook remainsconstructive.

The current slowdown should not be interpreted as weakness, but rather as a transition toward a more mature investmentenvironment, characterized by:

As a result, the companies that secure funding in this environment are likely to be better positioned for long-term impact and scale.

Q1 2026 confirms a clear shift in ConTech:

The market is no longer driven by experimentation at scale, but by execution with discipline.

Capital is still flowing—but with intent.

Innovation is still accelerating—but with accountability.

And ultimately, the winners will be those able to translate technology into measurable outcomes across the constructionvalue chain.

Cement is responsible for a significant share of global CO₂ emissions, commonly estimated at around 7–8%, according to the International Energy Agency and the Global Cement and Concrete Association. This is not a marginal footprint. It places cement among the most emissions-intensive industrial sectors worldwide.

What makes cement particularly difficult to decarbonize is the dual origin of its emissions:

As a result, decarbonizing cement is not simply a matter of switching to renewable energy. It requires rethinking both the chemistry and the industrial processes that underpin production.

Cement production is constrained by a combination of physical, chemical, and economic factors that limit the pace of transition.

Key challenges include:

According to the International Energy Agency, cement is classified as a “hard-to-abate” sector precisely because emissions are embedded in both energy use and industrial processes.

Decarbonization, therefore, requires systemic change—not incremental optimization.

Across the industry, climate ambition is increasingly being translated into measurable and time-bound targets.

For example, Cemex has established a net-zero CO₂ target by 2050, supported by intermediate goals aligned with science-based methodologies. These targets reflect a broader industry shift toward accountability and transparency.

However, targets alone do not deliver decarbonization. The critical step lies in translating ambition into operational pathways:

This transition, from commitment to execution, is where most of the complexity resides.

There is no single solution capable of decarbonizing cement. Progress depends on the combination of multiple technological pathways.

Reducing clinker content is one of the most immediate and effective levers. This includes:

These approaches aim to reduce emissions while maintaining performance and durability.

Because process emissions cannot be fully eliminated, CCUS is widely considered a critical decarbonisation lever for the cement industry.

According to theGlobal Cement and Concrete Association , CCUS could reduce carbon emissions by 36%, potentially making it the largest lever to reduce the cement industry’s emissions.

However, several key challenges remain:

Energy-related emissions can be reduced through:

The Global Cement and Concrete Association highlights alternative fuels as one of the most advanced levers currently being deployed at scale.

Digital technologies contribute to emissions reduction and operational performance improvements by increasing efficiency and reducing energy consumption

While individually incremental, these improvements can deliver meaningful emissions reductions at scale.

Innovation in cement is no longer confined to large industrial players.

A growing group of Cemex Ventures portfolio companies is advancing decarbonization across the construction value chain, from low-carbon cementitious materials and carbon utilization to process optimization, alternative fuels, and embodied carbon intelligence. Together, these startups reflect a broader industry shift: decarbonization is no longer driven by a single breakthrough, but by a new generation of specialized technologies tackling emissions at multiple points across industrial operations and the built environment.

This transformation is unfolding against a well-established backdrop. Cement production is widely estimated to account for around 7–8% of global CO₂ emissions, while long-term demand is expected to remain resilient as urbanization and infrastructure development continue worldwide. In that context, the challenge is not whether the sector needs to decarbonize, but how quickly scalable solutions can be deployed across existing value chains.

Cemex Ventures’ portfolio offers a clear view of where that innovation is gaining traction. Carbon Upcycling and Terra CO2 are developing lower-carbon cementitious materials and alternatives to conventional supplementary cementitious materials, helping reduce clinker intensity and embodied emissions. Optimitive applies AI to optimize industrial processes in real time, improving efficiency and lowering energy consumption in heavy industry environments. WtEnergy is advancing waste-to-syngas technology to replace fossil fuels in high-heat industrial applications. And Vizcab enables more informed decision-making around embodied carbon, equipping construction stakeholders with the data needed to measure, manage, and reduce emissions across the building lifecycle.

One of the defining challenges in cement decarbonization is not the lack of innovation, but the difficulty of scaling it.

Key barriers include:

According to the International Energy Agency, scaling low-emissions technologies remains one of the primary bottlenecks in hard-to-abate sectors.

In this context, collaboration between industrial players, startups, and investors becomes essential.

Despite these challenges, progress is already underway.

Across the sector, companies are:

Industry roadmaps, including those from the Global Cement and Concrete Association, indicate that these levers are already contributing to emissions reductions, even if full-scale deployment remains in progress.

Decarbonizing cement will require the convergence of three critical elements:

No single innovation will define the transition. Instead, success will depend on how effectively multiple solutions are integrated within real-world industrial systems.

The path to net-zero cement will not be defined by isolated breakthroughs, but by the ability to scale and operate a portfolio of technologies under real economic and operational constraints.

To explore the technologies and startups shaping the future of low-carbon construction, visit the Cleantech Construction Map 2026.

Cemex Ventures has released the 2026 Construction Cleantech Map, highlighting startups and emerging technologies driving the next wave of sustainability innovation across the construction sector.

The new edition focuses on four strategic verticals aligned with Cemex’s evolving innovation priorities: Fuels & Energy, Novel Cementitious Materials, Carbon Capture, Utilization & Storage (CCUS), and Smart Operations & Digital. These areas represent key technological levers to reduce emissions across the construction value chain, complemented by new business models that boost operational efficiency and optimize financial performance along the way.

The Construction Cleantech Map 2026 provides a snapshot of the rapidly expanding ecosystem of startups that address some of the most pressing sustainability challenges in the industry —from next-generation low-carbon materials and carbon capture technologies to energy solutions and digital platforms with the ability to exponentially upgrade industrial operations.

The Fuels & Energy vertical highlights startups enabling cleaner and cost-efficient energy systems across construction materials production, including renewable energy integration, process electrification, industrial heat, waste heat recovery (WHR) and other energy optimization technologies.

Startups working on Novel Cementitious Materials are developing alternative binders and new production processes designed to significantly reduce the carbon footprint of cement manufacturing, one of the most emissions-intensive processes in the global construction industry.

Meanwhile, companies operating in the CCUS space are advancing technologies capable of capturing carbon dioxide emissions from industrial sources, and either storing them permanently or converting them into useful products, —including construction materials.

Finally, the Smart Operations & Digital category showcases startups applying data, advanced analytics, and artificial intelligence to improve operational efficiency, reduce resource consumption, and support data-driven decision making across cement plants, supply chains, and construction sites.

“The path to a low-carbon construction industry requires innovation across materials, processes, and operations,” said Alfredo Carrato, Investment Manager at Cemex Ventures. “The Construction Cleantech Map helps highlight the startups developing technologies that can accelerate this transition and support the industry’s decarbonization efforts.”

Through initiatives like the Construction Cleantech Map, Cemex Ventures continues to identify and engage with startups that support the construction sector’s shift towards more sustainable future. These efforts align with Future in Action, Cemex’s global sustainability program aimed at achieving ambitious decarbonization targets across its cement, concrete, and aggregates operations.

By mapping the most promising innovators across the cleantech landscape, the initiative provides visibility to startups and fosters collaboration between technology developers and industry stakeholders committed to transforming the built environment.

A decade of backing construction innovation has culminated in one of the most significant ConTech acquisitions of 2026.

Over ten years ago, Cemex Ventures had a clear vision: the construction industry needed a space where innovation could meet the capital, pilots, and corporate networks required to scale. That vision gave birth to the Construction Startup Competition (CSC) — the world’s largest startup challengededicated to the construction sector.

Created by Cemex Ventures alongside some of the most influential leaders in the industry, the CSC has grown across nine editions into the defining event ofthe global ConTech ecosystem. With more than 2,000 startups from over 80 countries and a network of co-organizers that includes companies such as Hilti, VINCI Group’s Leonard, NOVA by Saint-Gobain, Dysruptek, Zacua Ventures, Trimble, and Caterpillar, the competition is far more than a contest, it is a transformation platform for the most ambitious entrepreneurs in construction.

Winners don’t just walk away with recognition. They gain access to investment, global-scale pilot projects, and direct connections to the decision-makers ofthe industry’s largest companies. The story of Document Crunch is the most compelling proof yet of what that access can ultimately mean.

Founded in 2019 in Atlanta by Josh Levy, Adam Handfinger, and Adam Nadler, Document Crunch was built to solve one of construction’s most persistentand costly challenges: contract complexity. In an industry where a single misread clause can spiral into a million-dollar dispute, Document Crunch developedan AI platform purpose-built for construction — one capable of reading, analyzing, and flagging critical risk provisions across construction contracts, insurance policies, technical specifications, and other key project documents.

The solution goes well beyond risk identification. It automatically generates project playbooks, delay notifications, and risk summaries, dramatically reducingthe administrative burden on project teams. From its earliest years of operation, the company grew at an extraordinary pace — with revenues increasingapproximately 500% in a single year — and went on to be deployed across more than 10,000 projects, serving general contractors, subcontractors, owners, designers, and insurance carriers alike.

In November 2021, at the BuiltWorlds Venture East Conference in Miami, Document Crunch took the stage at the Construction Startup CompetitionPitchday alongside nine finalists from around the world. That year’s edition was co-organized by Cemex Ventures, Dysruptek, Ferrovial, GS Futures, Hilti, VINCI Group’s Leonard, and NOVA by Saint-Gobain, with a jury made up of senior executives from each organizing company.

Document Crunch walked away with the gold medal of the competition’s sixth edition. Their proposition — purpose-built artificial intelligence forconstruction, capable of transforming how the industry understands and manages contractual risk — stood out in a field of high-caliber finalists. Therecognition was far from merely symbolic: it opened doors, generated visibility among key industry investors, and firmly established the founding team’sreputation within the global ConTech ecosystem.

Behind every significant exit, there are investors who believed before anyone else. In Document Crunch’s case, two of those early believers were, fittingly, co-organizers of the Construction Startup Competition itself: Zacua Ventures and Dysruptek.

In 2022, Document Crunch closed a $4.6 million seed round led by Zacua Ventures, the early-stage venture capital fund focused on the built environment, with presence in San Francisco, Madrid, Singapore, and Mexico City. What makes this milestone particularly significant is that Document Crunch was, quite literally, Zacua Ventures‘ very first investment as a fund — a distinction the team acknowledged publicly with pride. Zacua’s founding partners — VivinHegde, Mauricio Tessi Weiss, and Juan Nieto — had followed Josh Levy and his team closely for years before committing capital, building a relationshipgrounded in transparency and a shared vision for the future of the sector.

Dysruptek, the corporate venture arm of Haskell and one of the CSC’s most active co-organizers, also participated in the seed round as a repeat investor, having backed Document Crunch even before that milestone raise. Their commitment was not purely financial: Dysruptek deployed the solution internallyacross Haskell’s own projects, becoming one of the earliest corporate validators of the technology.

The round also brought in Fifth Wall, Argonautic Ventures, GTM Fund, Blue Collar Capital, and Holt Ventures, assembling a syndicate of investors with uniqueperspectives across construction, proptech, and enterprise software.

Following the seed, Document Crunch continued its growth trajectory: a $9 million Series A led by Navitas Capital with continued participation from Zacua Ventures, followed by a $21.5 million Series B in 2024. At each stage, the original investors maintained their conviction in the team and the platform.

On April 2, 2026, Trimble announced it had signed an agreement to acquire Document Crunch. The goal of the transaction is to integrateDocument Crunch’s document intelligence and compliance automation capabilities into the Trimble® Construction ecosystem, enhancing existing workflowsacross project management and construction ERP systems.

According to Trimble, Document Crunch’s platform will serve as the “contractual rule set” — the intelligent DNA — of the entire Trimble Construction One(TC1) suite, automatically pushing critical obligations, compliance requirements, and payment terms into operational project delivery workflows. In practicalterms, this means that for the first time, contractual intelligence and operational execution will be natively connected within a construction platform at global scale.

The acquisition does not start from scratch. Document Crunch was already part of the Trimble Ventures portfolio and an active Trimble Marketplace partner, integrated with Trimble ProjectSight®. What the agreement signals is the full incorporation of Document Crunch’s technology and team into the core ofTrimble’s value proposition for the AECO sector. The transaction is expected to close in the second quarter of 2026.

Document Crunch’s journey, from finalist in Miami to acquisition by one of the construction industry’s most prominent technology companies , is preciselythe story the Construction Startup Competition was designed to make possible.

The CSC was never conceived as merely a contest. It was built as an ecosystem: a space where the industry’s leading corporations could identify the mostpromising entrepreneurial talent ahead of the curve, and where startups could gain access, from day one, to the corporate partners, investors, and pilotopportunities that would otherwise take years to reach. Document Crunch proves that model works end to end. The recognition at CSC 2021 created visibility. Co-organizers Zacua Ventures and Dysruptek translated that early belief into foundational capital. And a years-long relationship with the competition’sbroader ecosystem , including Trimble, also a CSC partner, culminated in one of the most meaningful acquisitions ConTech has seen this decade.

Ten years after its first edition, the Construction Startup Competition continues to do exactly what it set out to do: connect the future of construction withthose who have the power to make it real.

Follow our digital channels to be the first to discover what’s coming next. More updates on the Construction Startup Competition will be shared shortly.

Cemex Ventures has appointed Jesús Ortiz as Head of its corporate venture capital platform, with the aim of strengthening its focus on integrating proven technologies and scaling solutions with tangible industrial impact across the construction value chain.

The construction sector is undergoing a structural redefinition. Technological advancement, mounting productivity pressures, and climate urgency are reshaping how assets are designed, delivered, and managed at a global scale. In this evolving landscape, competitive differentiation no longer lies in experimentation, but in the ability to operationalize, integrate, and scale solutions within real-world environments.

Ortiz assumes leadership with a clear mandate: to help translate innovation into tangible competitive advantage by reinforcing the link between corporate strategy, operational execution, and long‑term value creation.

“True transformation occurs when technology moves beyond pilot stages and becomes embedded within the operating model. Our focus is straightforward: integrate capabilities, scale solutions, and deliver measurable impact in active environments,” said Jesús Ortiz, Head of Cemex Ventures.

Over recent years, Cemex Ventures has evolved into a global collaboration platform connecting corporates, entrepreneurs, and investors with the shared objective of modernizing the built environment and strengthening its resilience.

As part of Cemex’s broader transformation, Cemex Ventures plays a strategic role in supporting the company’s long‑term objectives by identifying, integrating, and scaling technologies that are intended to strengthen operational performance, efficiency, and sustainability across Cemex’s global footprint. From its position within the organization, Cemex Ventures aims to contribute to the future of Cemex by enabling scalable innovation that supports competitiveness and long‑term value creation for shareholders.

Under Ortiz’s leadership, the strategy will focus on:

This leadership transition reinforces Cemex Ventures’ ambition to act as a catalyst for structural transformation within the industry. The emphasis is clear: innovation is not an end in itself, but a lever to enhance competitiveness, efficiency, and long‑term sustainability.

The sector’s evolution will not be defined by passing trends, but by disciplined execution, strategic integration, and scalable impact.

Cemex Ventures reaffirms its commitment to seeking to build operational transformation through action.