The third quarter of 2025 has rewritten the rules of the game for investment in construction technology (Contech) and Cleantech. Despite a slight dip in the number of transactions, the sheer volume of capital invested skyrocketed, driven by significant late-stage rounds.

Table of Contents

Key Takeaways (Executive Summary)

- Dramatic Capital Surge: Investment volume climbed a remarkable +89% compared to Q3 2024, reaching $1,513.4 million

- North American Dominance and Automation: The U.S. concentrated 80% of the capital. By vertical, Construction’s Future led the investment, fueled by automation and robotics solutions.

- The AI Effect: Adapt or Die: A surprising 83% of deals involved startups leveraging Artificial Intelligence, solidifying its role as the essential, cross-cutting technology in the sector.

- Setback in Green Construction: The Green Construction vertical saw a slowdown, capturing only 2% of the total capital, though there is growing activity in cleantech solutions intersecting with the built environment.

- The Impact of Strategic Investors: While strategic investors (corporates or CVCs) only participated in 15 deals (out of 75), they represented a significant 44% of the quarter’s invested capital.

Overall Market Analysis

Q3 2025 recorded a total of 75 transactions. While this represents a -10% decrease in the number of deals compared to Q3 2024, the total capital mobilized was historically high, reaching $5,963.4 million.$1,513.4 million. This significant increase demonstrates that, while the capital environment remains selective, funding is also allocated into mature, when solutions offer high-impact and value.

It is worth highlighting two acquisitions which, although not included in our analysis, deserve special mention: CRH’s $2.1B acquisition of Eco Materials and Verisk’s $2.35B acquisition of Acculynx

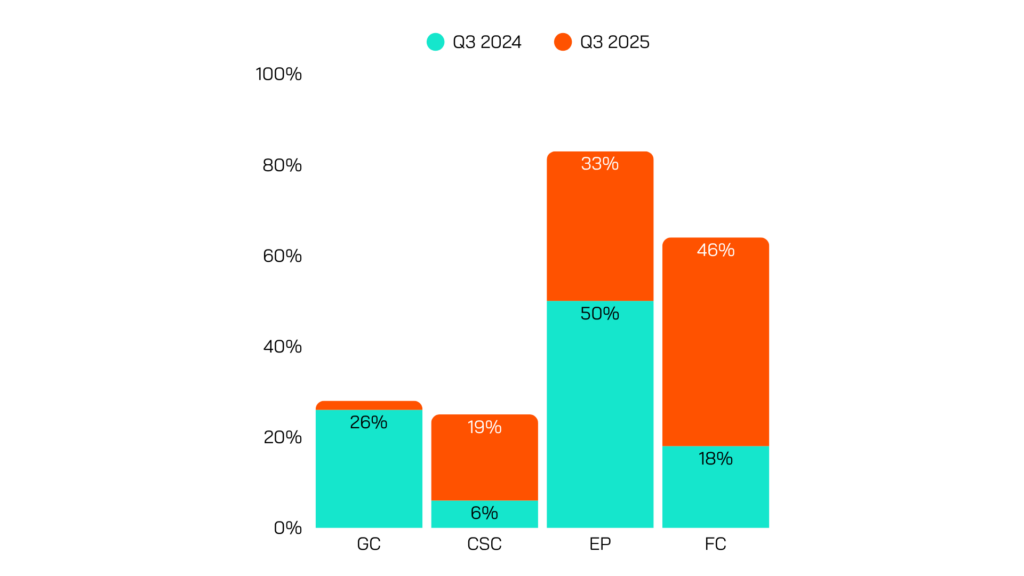

Investment by Focus Area

The distribution of underscores a clear preference for large-scale efficiency and technologies that are redesigning the construction value chain.

Vertical | % of Total Invested Volume | Key Insight |

Future of Construction | 46% | Leads investment, focused on automation and disruptive technologies. |

Enhanced Productivity | 33% | Solutions optimizing project management and operational efficiency. |

Supply Chain | 19% | Continued investment in material logistics and platform solutions. |

Green Construction | 2% | Captured only $33M across 9 transactions, indicating a slowdown. |

Construction’s Future solidified its position as the primary destination for capital, with a particular emphasis on automation and robotics for job sites.

In contrast, the Green Construction vertical experienced a noticeable slump. Despite the drop in investment volume for this vertical, trends indicate growing activity in cleantech solutions that intersect with the built environment (e.g., building energy management and industrial decarbonization).

The common thread linking all verticals is Artificial Intelligence: 83% of the deals involved startups applying AI in their business models, reinforcing the industry’s mantra: “Adapt or die to stay competitive.”

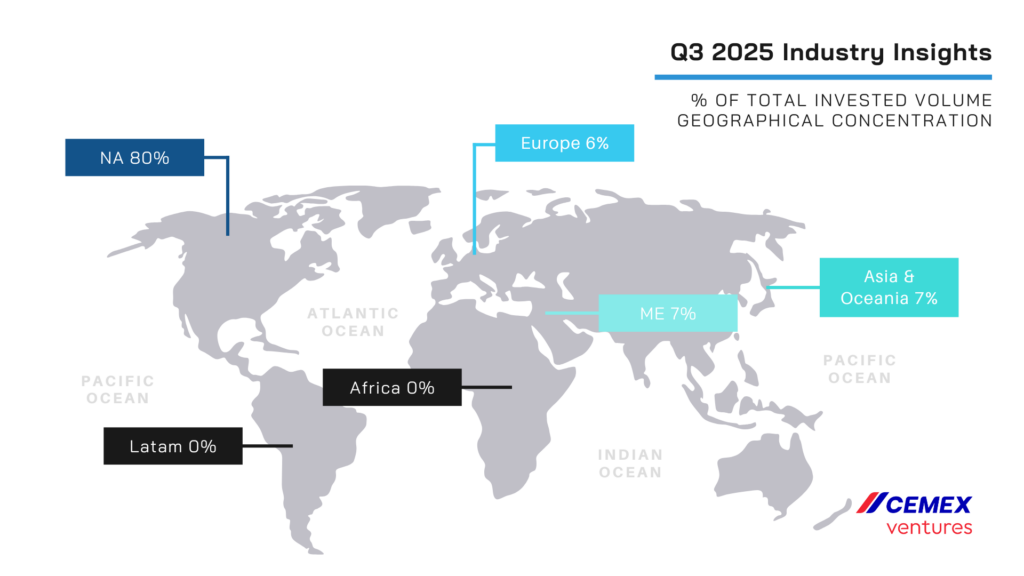

Geographic Concentration

The global Contech market remained heavily concentrated in North America, an unbroken trend that continues to set the pace for the ecosystem.

The U.S. Dominance: Within North America, the United States was the main engine, accounting for an overwhelming 80% of total transactions, deploying $1.21 billion across 42 deals in the quarter.

Key Deals and the Strategic Role

Q3 2025 was characterized by the maturation of capital, reflected in several high-volume, late-stage transactions:

- FieldAI: Secured $400M in Growth Rounds in August 2025. This capital, raised in two consecutive rounds, is earmarked to accelerate the company’s global expansion and advance Embodied AI at scale for physical robotics. Read more

- Infra.Market: Finalized $150M in Debt plus $83M in Equity (Late-Stage Funding) in July 2025. The funding will be used to fuel the company’s global ambition and strategic growth in its building materials platform. Read more

- Motive: Raised $150M in Growth Funding in July 2025. The investment, led by Kleiner Perkins, supports the continued growth of its AI-powered fleet management and operations platform. Read more

- SpeedChain: Secured $111M in Equity and Debt Financing in September 2025. This mix of funding will be used to expand its fintech solutions for business expense management and corporate credit cards. Read more

- Exodigo: Closed a $96M Series B round in July 2025. The capital will be channeled into expanding its global team and accelerating the development of its AI-powered subsurface mapping platform. Read more

- PassiveLogic: Raised $73M in a Series C Round during Q3 2025. This investment bolsters its platform for autonomous building systems and energy efficiency. Read more

- Bedrock Robotics: Emerged from stealth with $80M in combined Seed and Series A funding in July 2025. The company will use the funds to develop autonomous systems that retrofit existing construction equipment. Read more

The Power of Strategic Investors

A key highlight of the quarter was the disproportionate influence of Strategic Investors (corporates or CVCs). Although they only participated in 15 deals, these transactions represented a significant 44% of the total net invested capital. This data underscores that construction and industrial firms are using their VC arms to make large, definitive bets on solutions they deem essential for their future success.