Table of Contents

By the Cemex Ventures Investment Team | July 2026

The construction technology (ConTech) investment landscape delivered a strong signal in the second quarter of 2026: capital is back in motion. After a cautious start to the year, Q2 2026 closed with $1.031 billion in disclosed investment volume across 84 transactions, a 30% increase in deployed capital compared to Q2 2025. This resurgence, concentrated in productivity-enhancing technologies and AI-native startups, reflects a market that is becoming more selective, more strategic, and increasingly convinced that artificial intelligence is not a trend but a foundational transformation for the built environment.

At Cemex Ventures, we track global ConTech investment flows every quarter to map where innovation capital is going, and what it tells us about the future of construction. This report covers Q2 2026 data and full H1 2026 context, surfacing the key themes, geographies, and deal dynamics shaping the industry right now.

Q2 2026 at a Glance: More Capital, Fewer Deals

The headline numbers from Q2 2026 tell an interesting story. Investment volume jumped 30% year-over-year to just over $1 billion, yet the number of transactions fell 8%, from 92 deals in Q2 2025 to 84 in Q2 2026. This divergence between capital deployed and deal count points to a broader industry dynamic: investors are concentrating more capital into fewer, more mature bets. Check sizes are growing, diligence bars are rising, and the speculative flurry of earlier years has given way to conviction-driven deployment.

This is not a sign of weakness. It is a sign of maturity.

” ConTech deal activity remains within historical parameters and should not be interpreted as a sign of weakness. While transaction volume has declined compared to last year, we do not observe any meaningful market contraction. Instead, this moderation may be an indication of a maturing ecosystem, where investors are becoming more selective and concentrating capital in higher-quality opportunities. Overall, current activity levels remain healthy and do not raise concerns about the underlying strength of the sector. “ — Miguel Carralón, Investments & Partnerships Manager, Cemex Ventures

The ConTech ecosystem is shedding the excess of the 2021–2022 boom cycle and rebuilding around companies that can demonstrate real revenue, measurable ROI, and genuine product-market fit. The investors still writing checks, and they are writing larger ones, believe in the long-term thesis: construction is one of the world’s largest and least digitized industries, and the window to back the companies that will transform it remains wide open.

H1 2026 in Full Context: $2.884B Across 153 Transactions

Zooming out to the full first half of 2026, total disclosed investment volume reached $2.884 billion across 153 transactions. On the surface, this represents a 19% decline in invested capital and a 20% drop in deal count versus H1 2025. But surface-level numbers require context.

Critically, the $2.884B figure excludes at least three major undisclosed acquisitions completed during the first half of the year. Incorporating reasonable estimates for these transactions, total H1 2026 investment volume is likely closer to $4.5 billion. The reduction in deal activity is real, but 153 transactions across six monthsreflects a healthy, active market.

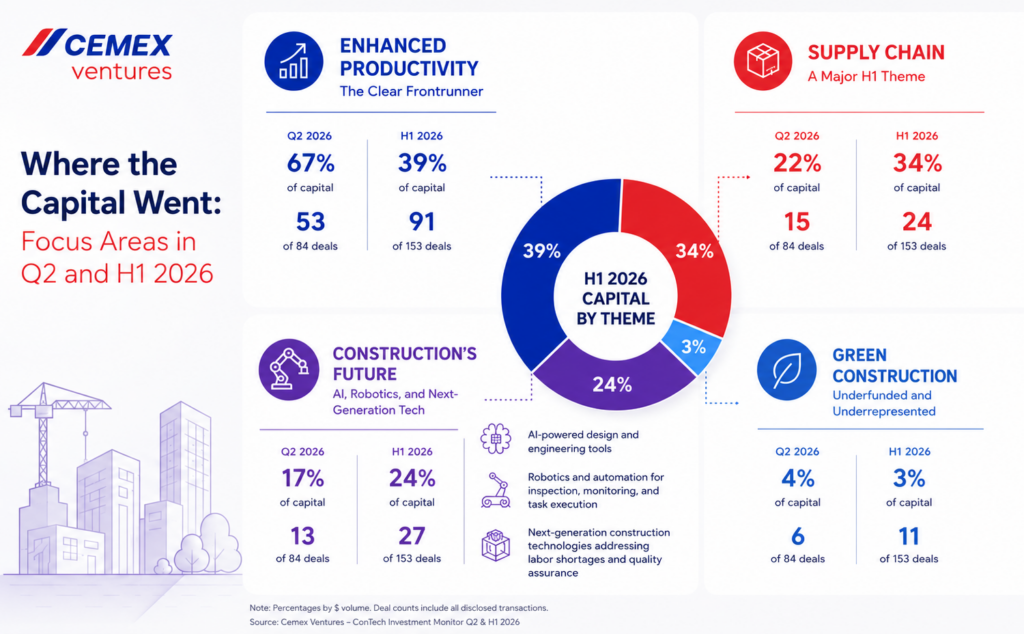

Where the Capital Went: Focus Areas in Q2 and H1 2026

Enhanced Productivity: The Clear Frontrunner

The dominant investment theme of Q2 2026, and the entire first half, was Enhanced Productivity. This category captured 67% of Q2 investment volume by dollar amount and 39% of H1 2026 capital. By deal count, Enhanced Productivity accounted for 53 of 84 transactions in Q2 and 91 of 153 in H1.

Investors are backing platforms that improve efficiency, automate repetitive workflows, digitize project execution, and reduce rework on construction sites. The appetite here is enormous, and it is easy to understand why: construction productivity has stagnated for decades relative to other industries. The companies solvingthis problem, whether through project management software, AI-powered scheduling, or digital twins, are addressing a genuine and urgent pain point for owners, contractors, and developers worldwide.

Supply Chain: A Major H1 Theme

Supply Chain technologies emerged as the second-largest investment category in H1 2026, capturing 34% of invested capital and 24 transactions over the six month period. This reflects a sustained wave of investment in logistics optimization, procurement digitization, materials tracking, and supplier network management.

The construction supply chain remains one of the most fragmented and opaque in any major industry. Material delays, cost overruns, and lack of real-time visibility have long plagued projects at every scale. The startups attracting capital here are applying AI and data infrastructure to make the supply chain predictable, transparent, and responsive, capabilities the industry desperately needs.

“Supply chain is where projects are won or lost long before anyone sets foot on a jobsite. The surge of investment in this space reflects a growing understanding that digitizing procurement and logistics isn’t optional , it’s a competitive necessity for any serious contractor or developer.” — Jose Antonio Brunet, Principal, Cemex Ventures

Construction’s Future: AI, Robotics, and Next-Generation Tech

The Construction’s Future category, encompassing AI-native design tools, robotics, autonomous systems, and advanced manufacturing, represented 17% of Q2 investment volume and 24% of H1 capital. With 13 deals in Q2 and 27 across H1, this category is punching above its weight in terms of strategic significance.

Three investment sub-themes stand out: AI-powered design and engineering tools that accelerate blueprint generation, optimize space utilization, and help ensure regulatory compliance; robotics and automation for inspection, monitoring, and task execution on jobsites; and next-generation construction technologiesaddressing labor shortages and quality assurance. These are the technologies that will define construction over the next decade.

Green Construction: Underfunded and Underrepresented

Green Construction captured just 4% of Q2 investment volume (6 transactions) and 3% of H1 capital (11 deals). For an industry under significant pressure to decarbonize, and a regulatory environment in Europe and beyond that is tightening fast, this allocation remains strikingly low.

The opportunity is clear. The capital is not following it yet. This gap between sustainability imperative and investment reality is one of the defining tensions in ConTech right now, and one we expect to close as carbon reporting requirements, ESG mandates, and green procurement standards become unavoidable.

“Green Construction is still waiting for its inflection point. The regulatory pressure is mounting particularly in Europe; and the corporate sustainability commitments are real. The question is not whether capital will flow into this space, but when.” — Miguel Carralón, Investments & Partnerships Manager, Cemex Ventures

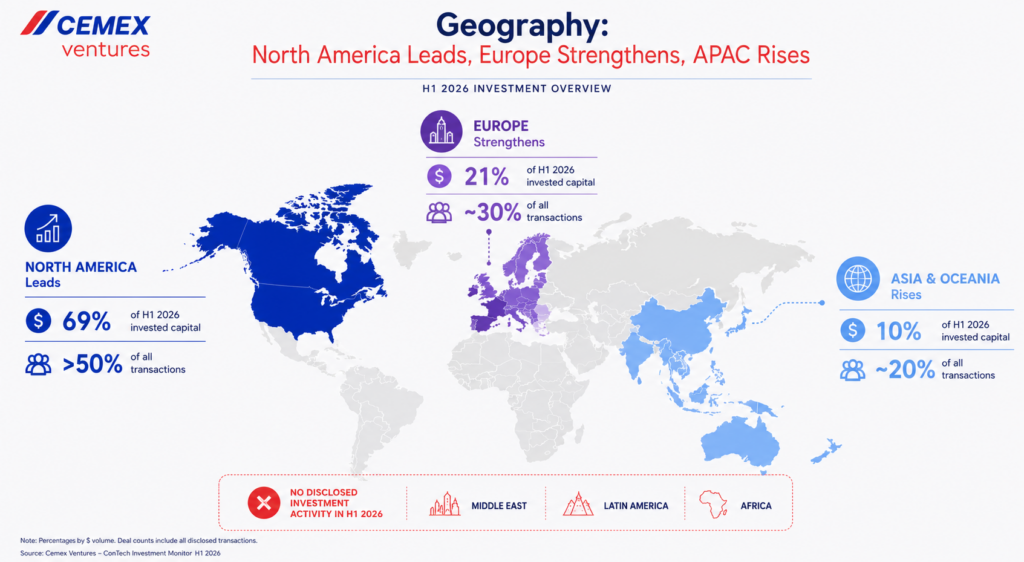

Geography: North America Leads, Europe Strengthens, APAC Rises

From a geographic perspective, the investment landscape remains heavily concentrated in three regions.

North America dominated H1 2026 with 69% of total invested capital and slightly more than half of all transactions. The U.S. market continues to lead in deal activity, check size, and the density of mature ConTech companies approaching growth and late-stage rounds. The concentration of strategic corporate investors and institutional venture capital in North America gives the ecosystem structural advantages that are difficult to replicate elsewhere in the short term.

Europe ranked second, attracting 21% of H1 invested capital and close to 30% of all deals. The gap between Europe’s share of capital (21%) and its share of deal count (approximately 30%) reflects smaller average deal sizes, but also a vibrant, diverse startup ecosystem spanning the UK, Germany, the Nordics, France, and the Iberian Peninsula. European ConTech continues to attract both local and cross-border investors, and the region’s strong regulatory push around sustainability and digitization is creating tailwinds for startups in green construction, compliance tech, and supply chain management.

Asia and Oceania accounted for 10% of H1 investment volume but nearly 20% of transactions, a pattern consistent with smaller deal sizes and a very active early-stage startup environment. Markets including Australia, Japan, Singapore, and India are generating significant entrepreneurial activity in construction digitization, and investor engagement in the region is deepening.

Notably, the Middle East, Latin America, and Africa recorded no disclosed investment activity in H1 2026. This does not necessarily mean deal activity is absent, it reflects limited public disclosure, but it does underscore the continued concentration of the tracked ConTech investment universe in three core geographies.

Stage Distribution: Early-Stage Optimism Prevails

The breakdown of H1 2026 transactions by round type confirms that early-stage investing continues to dominate ConTech. Approximately 70% of all deals fell between Pre-Seed and Series A (108 transactions), while the remaining 30% corresponded to growth and later-stage rounds: 15 Series B, 2 Series C, 8 late-stagetransactions, 9 M&A deals, and 11 classified as other.

This distribution has two important implications. First, investors remain excited about the long-term opportunity in construction technology and are actively seeding the next generation of solutions, even as the overall funding environment has become more selective. Second, the pipeline of companies moving from early togrowth stage will determine whether H1 2026’s early-stage enthusiasm translates into a robust mid-stage ecosystem in 2027 and 2028.

The M&A activity is equally notable. Nine disclosed acquisitions in H1 2026 signal that the consolidation phase in ConTech is well underway, as larger platform players absorb specialized capabilities to strengthen their product suites.

The M&A Signals: Procore, Autodesk, Trimble — and a $3.6B Headline

Three strategic acquisitions during H1 2026 deserve particular attention because they reveal the strategic priorities of the industry’s largest platform providers.

Procore acquired DataGrid. Autodesk acquired Rhumbix. Trimble acquired Document Crunch. In all three cases, the acquirer targeted an AI-native company to strengthen a critical segment of its platform and embed artificial intelligence more deeply into construction workflows. These are not defensive acquisitions, they are offensive moves by companies that recognize AI integration as a competitive necessity.

And then there is the headline transaction of the period: Autodesk’s announced intention to acquire MaintainX for approximately $3.6 billion. This deal is a statement of strategic intent. Autodesk is no longer content to own design and preconstruction workflows; it wants to extend its platform into operations, facilitiesmanagement, asset lifecycle, and Industrial AI. For a company that has historically lived in the design phase, MaintainX gives Autodesk a credible foothold in the operational world that follows. If completed, this acquisition could fundamentally redefine Autodesk’s addressable market and intensify platform competitionacross the full construction lifecycle.

The AI Inflection Point: 70% of Deals Are AI-Enabled

Perhaps the most striking data point from H1 2026 is this: approximately 70% of all ConTech transactions involved AI-enabled startups. This figure is not incidental, it is structural.

AI has stopped being a differentiator and started being a baseline expectation. Across Enhanced Productivity, Supply Chain, Construction’s Future, and even Green Construction, AI capabilities are being embedded into the core product architectures of the most fundable companies. Investors are no longer asking “does thisuse AI?” They are asking “how deeply is AI integrated, and how defensible is the resulting moat?”

Importantly, AI is not a separate vertical in ConTech, it is an enabling layer that cuts across every category. This distinction matters for how investors think about portfolio construction and how founders position their companies.

“We no longer evaluate startups by asking whether they use AI. We evaluate them by asking how central AI is to their defensibility. A company that has bolted on a chatbot is very different from one that has built its entire data and product architecture around AI capabilities from day one.” — Jose Antonio Brunet, Principal, Cemex Ventures

Strategic Investors Reach Record Participation

One of the most consequential trends in H1 2026 was the record level of participation from strategic corporate investors, who joined 37% of all transactions during the period. This is the highest level of corporate venture and strategic co-investment activity the ConTech market has seen.

Strategic investors, including construction companies, materials manufacturers, real estate developers, and engineering firms, bring more than capital to the table. They provide distribution, pilots, domain expertise, and market credibility that financial investors cannot replicate. Their growing presence signals that theconstruction industry itself is becoming a more active participant in shaping its own technological future, not merely a passive customer of innovation.

Where are strategics placing their bets?

The three investment themes gathering the interest from stratic investors are: project management and workflow optimization platforms that improve collaboration and data flow across the construction value chain; robotics and automation systems for inspection, monitoring, and task execution on active jobsites; and AI-powered design and engineering toolsthat accelerate blueprinting, support regulatory compliance, and optimize material consumption.

For startups, landing a strategic investor at an early stage has become a meaningful validation signal. For the ecosystem, it accelerates the path from pilot to deployment and helps close the gap between promising technology and real-world adoption.

What Q2 and H1 2026 Tell Us About the Road Ahead

Reading the Q2 and H1 2026 data together, several conclusions emerge:

The ConTech market is consolidating around quality. Fewer deals with larger check sizes reflect a flight to conviction. Companies that can demonstrate traction, unit economics, and scalability are attracting capital; those that cannot are finding the environment significantly harder.

AI is now the price of admission. Seventy percent AI penetration across transactions is not a coincidence. The companies raising capital are, in most cases, AI-native or AI-integrated by design. This will only accelerate.

Productivity, supply chain and new construction methods will remain the core investment thesis. Together, these categories accounted for amost all H1 capital. They address the industry’s most immediate and measurable pain points, and the total addressable market for both remains enormous.

Green Construction needs a catalyst. With 3% of H1 capital, sustainability-focused ConTech is significantly underfunded relative to the urgency of the decarbonization challenge. Regulatory pressure, net-zero commitments from major owners and developers, and maturing carbon accounting standards may provide thatcatalyst in H2 2026 and beyond.

The M&A wave is real and accelerating. The Autodesk-MaintainX deal alone represents a potential $3.6B transaction. Combined with the Procore, Trimble, and other strategic acquisitions, the platform consolidation narrative is becoming one of the defining stories in construction technology.

At Cemex Ventures, we remain committed to tracking, analyzing, and participating in the ConTech investment ecosystem. Q2 2026 confirmed what we have long believed: the construction industry is at an inflection point, and the companies building the technologies that will define its future are raising capital, findingcustomers, and scaling faster than ever.

The next wave of construction innovation is not coming. It is already here.